The long-end of the yield curve is jumping in bear-steepening fashion following yesterday’s hawkish 25-bp cut from the Federal Reserve. The central bank noted that the trim was a close call, with some non-voting members preferring a pause and Cleveland Fed President Beth Hammack formally dissenting. Stocks sold off hard, particularly the rate-sensitive small-cap segment, which had been counting on a speedy walk down the monetary policy stairs. But Chair Powell noted heightened trade and geopolitical uncertainty that warrant slower adjustments as the Trump administration arrives in Washington next month. Meanwhile, the BoJ and BoE held rates steady, while the stateside economic calendar depicted an upward revision to US GDP, which was met with better-than-expected figures on unemployment claims and existing home sales. Markets are responding in a mixed way, with stocks barely clawing back some of yesterday’s massive losses while the dollar makes a 25-month high, helped by loftier long-end yields, favorable interest rate differentials and expectations of US outperformance on a relative basis.

Fed Pencils In More Inflation

The Fed upwardly revised its forecasts on economic growth, inflation and the neutral rate of interest while downwardly adjusting its projection for unemployment in response to much stronger economic data published recently. Chair Powell reflected caution in his presentation following the released materials, a separation from his recent behavior of appeasing market participants during presentations. Powell spoke about the need to go slow in light of price pressures beginning to tick higher, which upset markets which were counting on continued friendliness from the central bank. Indeed, an agitated Fed is a headwind to equity valuations and term premium at the long-end of the curve, which comes as a shock considering that the committee was in such a rush to cut 50-bps in September when it cited decelerating employment conditions but is now patient in light of cloudy price pressure expectations. The policy error from September opened the door to the mistake yesterday, because the central bank wouldn’t have been perceived positively from a credibility perspective if it paused in December after having cut in super-sized fashion just three months ago.

Growth Revised Higher on Heels of FOMC

This morning’s final revision to US Gross Domestic Product (GDP) upgraded the third quarter growth rate to 3.1% from 2.8%. The revision marks an acceleration from the second quarter’s 3% clip and is the quickest pace of advancement since fourth quarter 2023, when growth hit 3.2%. The positive surprise was driven by stronger figures on exports and consumer spending that were partially countered by private inventory investment and imports. Corporate profits were adjusted south to a quarterly contraction of 0.4%, however, pointing to the possibility for earnings weakness ahead.

Past performance is not indicative of future results

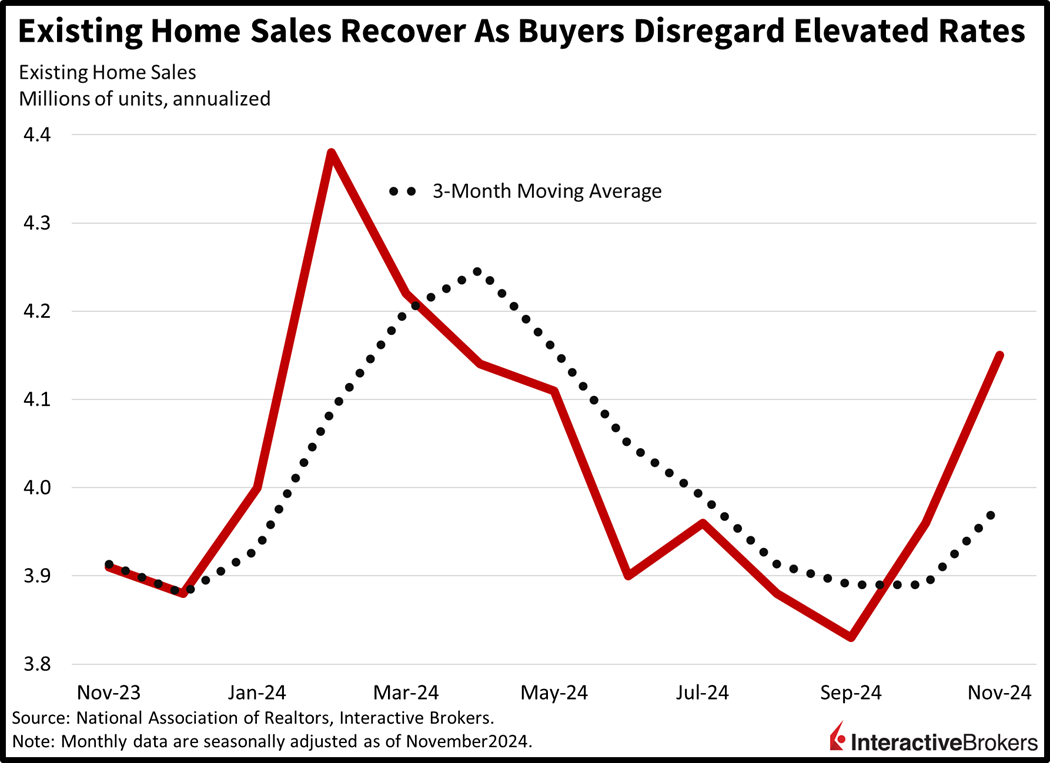

Existing Home Sales Climb Again

Home shoppers appear to have finally bitten the bullet of high financing costs and sticker shock, with existing home sales increasing for the second-consecutive month in November, according to the National Association of Realtors. The 4.8% month-over-month (m/m) increase resulted in a seasonally adjusted annualized rate of 4.15 million, up from 3.96 million in the October. Economists expected an annualized pace of 4.09 million. In November, inventory declined 2.9% while prices rose 4.7% year over year (y/y) to another all-time high amidst broad participation in transaction growth from single-family, condominiums and cooperatives as well as within all four regions except for the West, which was unchanged.

Past performance is not indicative of future results

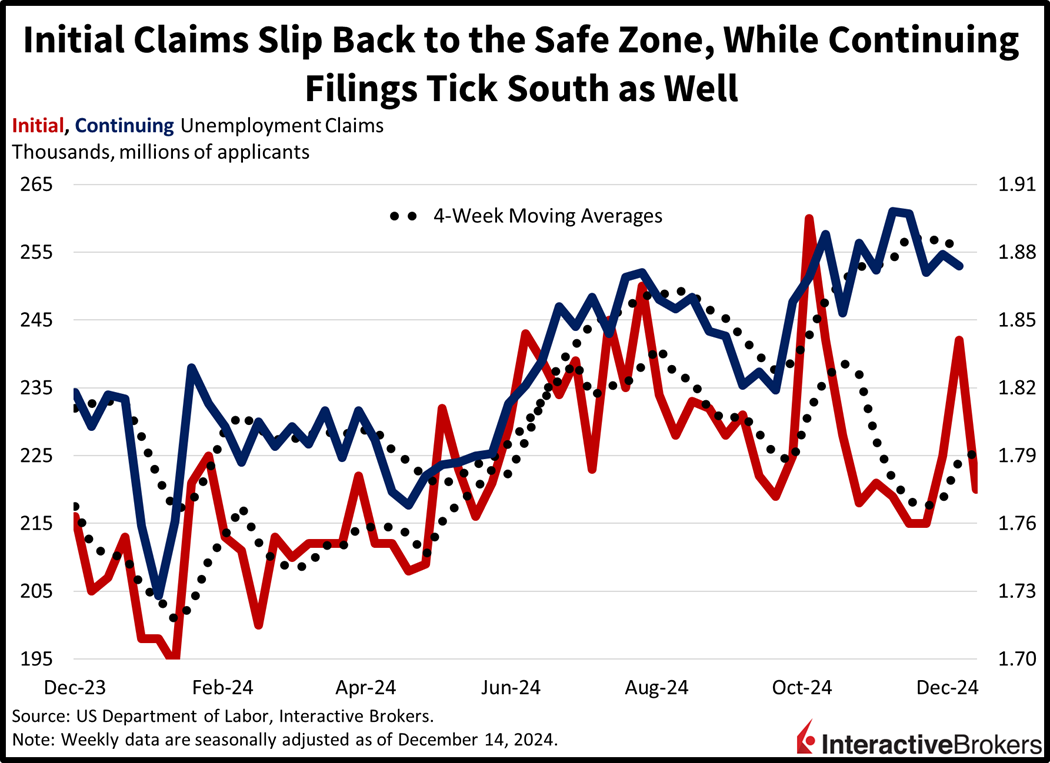

Initial Unemployment Claims Ease

After recently hitting a two-month high, initial unemployment claims dropped significantly for the week ended Dec. 14 while the difficulty that out-of-work individuals experience when seeking to get hired moderated. First-time requests for benefits fell from 242,000 to 220,200, below the estimate of 229,000 and back into the safe zone. Continuing claims, which serve as a proxy for the ease, or lack of ease, that idle Americans face when seeking work, dropped from 1.879 million to 1.874 million for the week ended Dec. 5. Wall Street expected the metric to increase to 1.890 million. While claims data can be volatile, four-week moving averages depict mixed results. The averages for initial and continuing claims changed from 224,250 and 1.886 million, respectively, to 225,500 and 1.880 million.

Past performance is not indicative of future results

PC Sales Weaken

Micron (MU) shares fell more than 15% this morning after the company provided weak guidance, citing an industry glut of dynamic random-access memory (DRAM) and soft consumer appetites for computers. On a positive note, however, Micron said its version of DRAM products for artificial intelligence, or high-bandwidth memory (HBM) chips, is experiencing strong demand. For the recent quarter, earnings exceeded expectations while revenue was in-line with forecasts.

Homebuilder Lennar Homes (LEN) reported a 9% y/y decline in revenue, explaining that high mortgage rates are hindering sales. Both revenue and earnings missed analysts’ expectations. During the recent quarter, home deliveries fell 7% and the average sales price sunk 2.5%. It expects current-quarter new orders to range from 17,500 to 18,000, which is below analyst expectations. Lennar shares dropped 4.5% following the earnings release.

Yen Hits Four-Month Low

In Asia, the Bank of Japan (BoJ) chose to hold rates at 0.25% and Governor Kazuo Ueda’s remarks drove the yen south to a four-month low alongside rate hike projections. Market participants are now expecting that the third interest bump in the current hiking cycle may occur as late as March. Ueda, similar to Powell and the FOMC, citied significant risk regarding the outlook for global trade and goods inflation next year. He is also awaiting compensation data from Tokyo to further guide the institution’s march up the monetary policy stairs. Meanwhile, board member Naoki Tamura was the only participant who supported a quarter-point hike, which marked a change from the unanimous decision in October. Furthermore, new prime minister Shigeru Ishiba and his minority government, that has a hawkish bias, are working with leaders of the opposition, who are more reluctant to tighten monetary policy in order to achieve consensus of the proper path of rates.

UK Maintains Key Rate

The Bank of England (BoE) also chose to keep rates at their current level. But three of nine voting members supported a reduction to 4.5%, despite the market only expecting one policymaker to favor such a change. British central bankers are highly attentive to elevated services inflation, shelter costs and wage growth. The central bank forecasts no economic growth this quarter, a downward adjustment relative to its 0.3% rate expected last month. Governor Andrew Bailey said the world is too uncertain to commit to a February rate cut at this juncture, but he pointed to the groundhog month as a reasonable starting point.

Dead-Cat Bounce

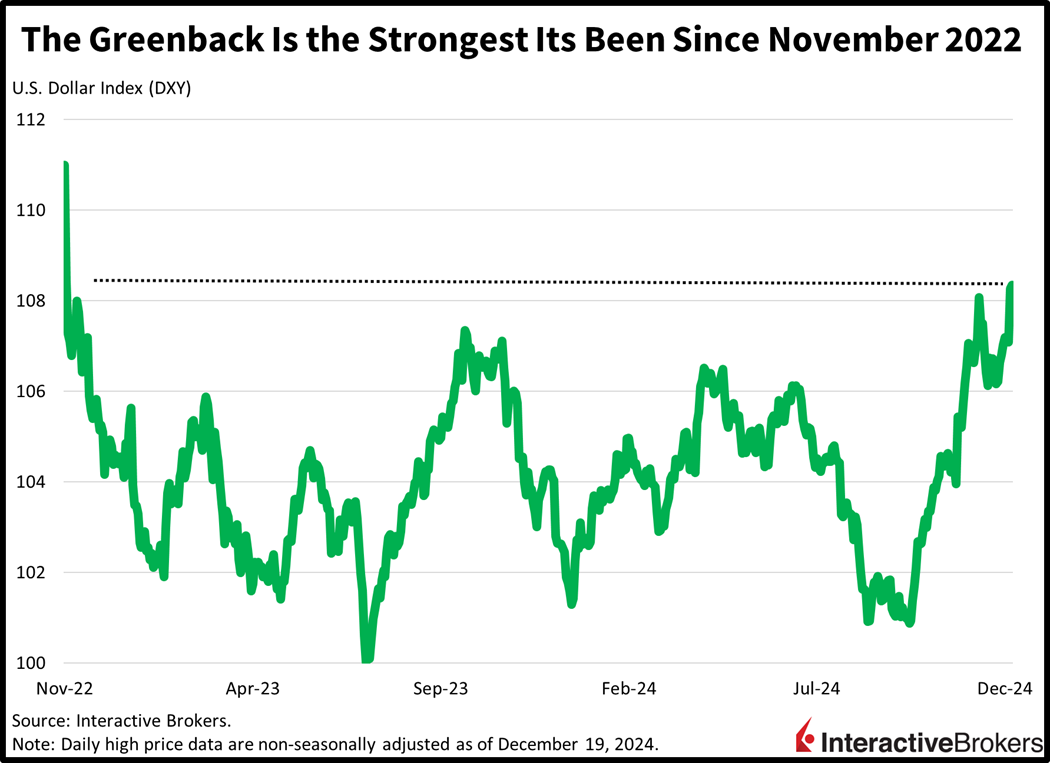

Markets are tilted bearishly with stocks trying to dead-cat bounce from yesterday’s selling pressure but failing to make much progress. Against this backdrop, the yield curve is steepening severely, with the short-end moving south while the long-end marches north. The dollar, meanwhile, is up to its highest level in over two years, as favorable interest rate differentials contend with domestic outperformance and Trump’s proposed tariffs, all of which support the greenback.

Turning back to stocks, major, domestic benchmarks are mixed, with the S&P 500 and Dow Jones Industrial indices up 0.4% each, the Nasdaq 100 at the flatline and the Russell 2000 down 0.3%. Sector breadth is also in the middle with 5 out of 11 segments gaining on the session and led higher by utilities, financials and technology, which are up 0.9%, 0.8% and 0.5%. The laggards, on the other hand, are represented by healthcare, materials, and real estate, which are losing 0.9%, 0.5% and 0.5%. In fixed-income, currencies and commodities, the 2- and 10-year Treasury maturities are changing hands at 4.29% and 4.56%, 7 basis points (bps) south on the former but 4 bps north on the latter. The Dollar Index is benefiting from a heavier long-end, trading at 108.28, a gain of 7 bps as the greenback appreciates relative to the yen, pound sterling and yuan but depreciates versus the euro, franc and Aussie and Canadian tenders. Commodities are mixed, with silver and copper lower by 1.8% and 0.3%, but lumber, crude oil and gold are higher by 0.4%, 0.1% and 0.2%. WTI crude is trading at $69.50 per barrel as demand uncertainty fueled by tighter monetary policy expectations and a stronger dollar limit price gains.

Past performance is not indicative of future results

Santa Rally Is Cancelled

As I write this conclusion, I’m getting déjà vu moments from 2022, when I wrote that the Santa Claus rally was cancelled. Well, unfortunately, the equity market’s ferocious valuation expansion was enabled by a friendly Fed, which has now turned into a foe. The Fed’s agitation, displayed yesterday, closes the door to further extension in earnings multiples and places the focus squarely on earnings, which have not advanced nearly as quickly as the stock market. Furthermore, the Fed’s apprehension and endless citations to uncertainty are swallowing up risk premiums, with the central bank’s messaging sending the 10-year yield to its highest level since May while the greenback climbs to its strongest height since November 2022, more than two years ago. Finally, a black swan event for the incoming year would be an interest hike by the Fed as price pressures return to a 3-handle, which would produce a much more volatile landscape than we’ve become accustomed to. Ladies and gentlemen, I believe the Santa Claus rally is cancelled this year, just like in 2022, as a lack of buying interest occurs against the backdrop of elevated valuations, driving volatility north and prices south.

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account