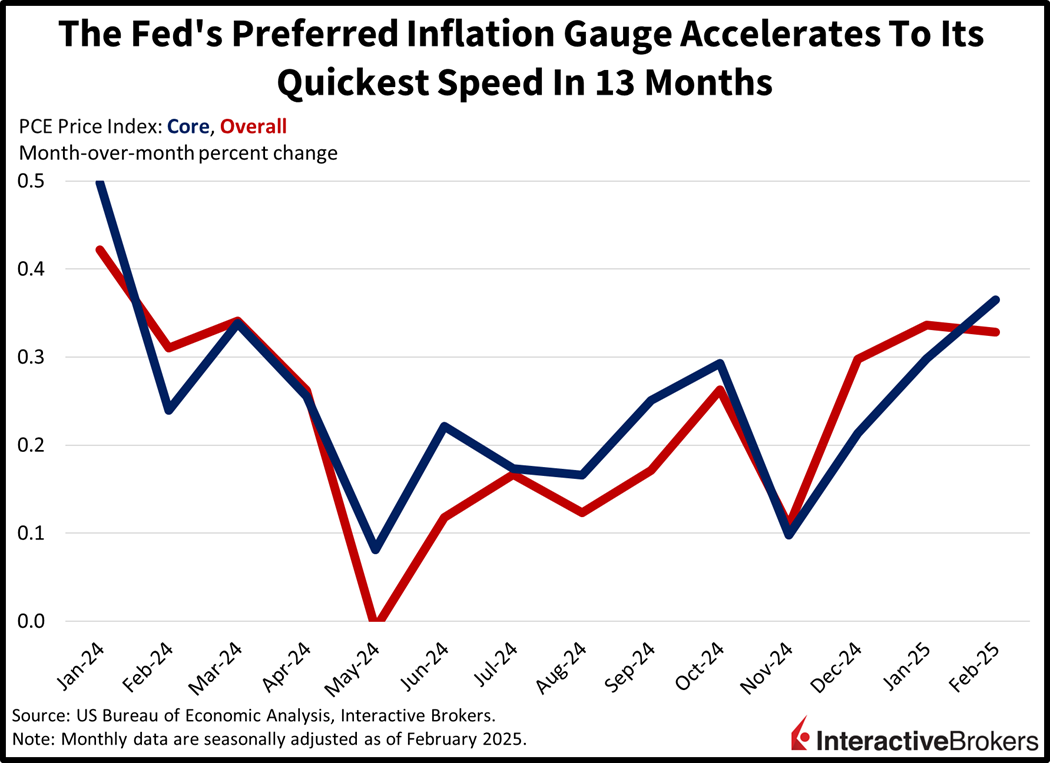

Recession fears are gripping Wall Street as this morning’s economic data confirmed that the consumer stumble in January, largely attributed to unfavorable weather conditions, extended into February. And with household expenditures striking out in the beginning months of 2025, first quarter GDP is likely to be negative unless shoppers came out charging in March. Meanwhile, the inflation numbers in the PCE print were unfriendly, as the Fed’s preferred core gauge accelerated to its fastest pace in 13 months while the durable goods category marked its quickest climb in 29 months. The stagflationary combination, arriving ahead of a broadening of Trump tariffs starting this Wednesday, is driving demand for safe-haven assets with traders flocking towards their bunkers. Investors are aggressively dumping stocks and greenback exposure in favor of long-dated Treasurys, gold bars, volatility call options, equity index put derivatives and forecast contracts. Furthermore, emblematic of the slowdown worries is the bull-flattening across the yield curve, as fixed-income watchers dial down growth expectations.

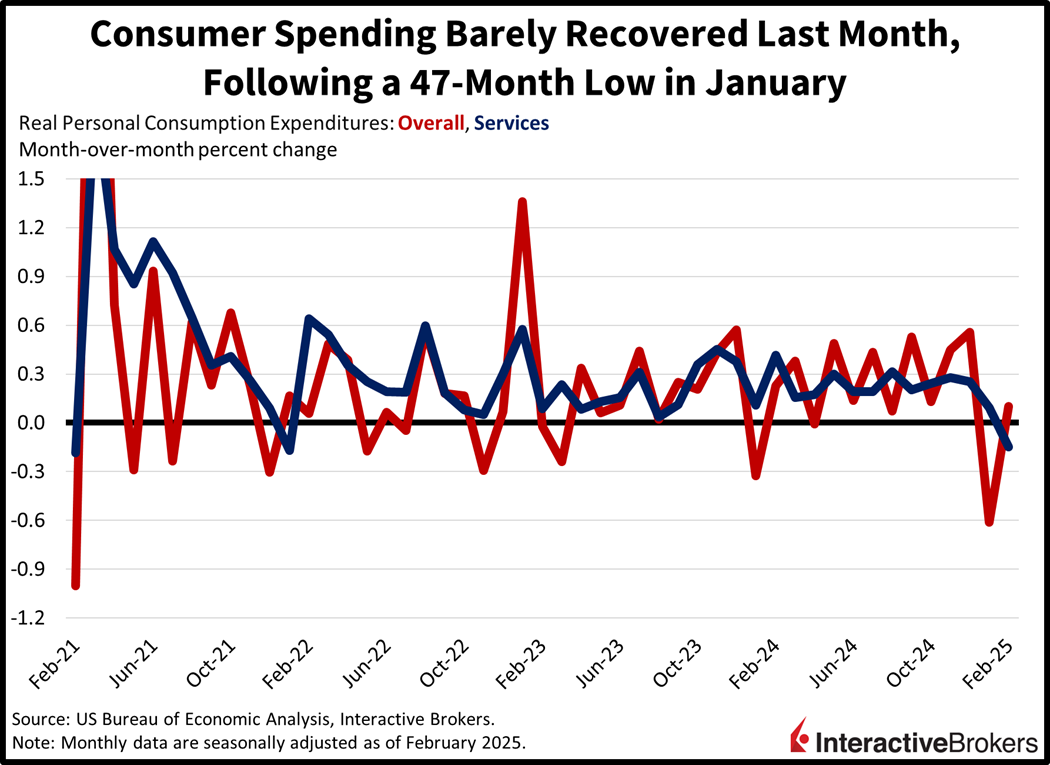

Consumers Post Another Weak Month

Consumer spending barely recovered in February after posting the sharpest monthly plunge in 47 to start the year. The pace of real consumption, which is adjusted for inflation, increased just 0.1% month over month (m/m), below the median estimate of 0.2% but better than January’s 0.6% drop. Despite shoppers increasing their purchases of durable and non-durable good volumes by 1% and 0.5% m/m, a 0.1% reduction in the significant services category countered those gains. The contraction in services was the steepest in 37 months, marking the first negative result since January 2022. On a positive note, strong wage growth pushed income up 0.5% after accounting for prices, stronger than the 0.1% projection and the 0.4% stride from January. The pullback in outlays alongside the jump in compensation generated a personal savings rate of 4.6%, an advancement from the prior period’s 4.3%.

Past performance is not indicative of future results

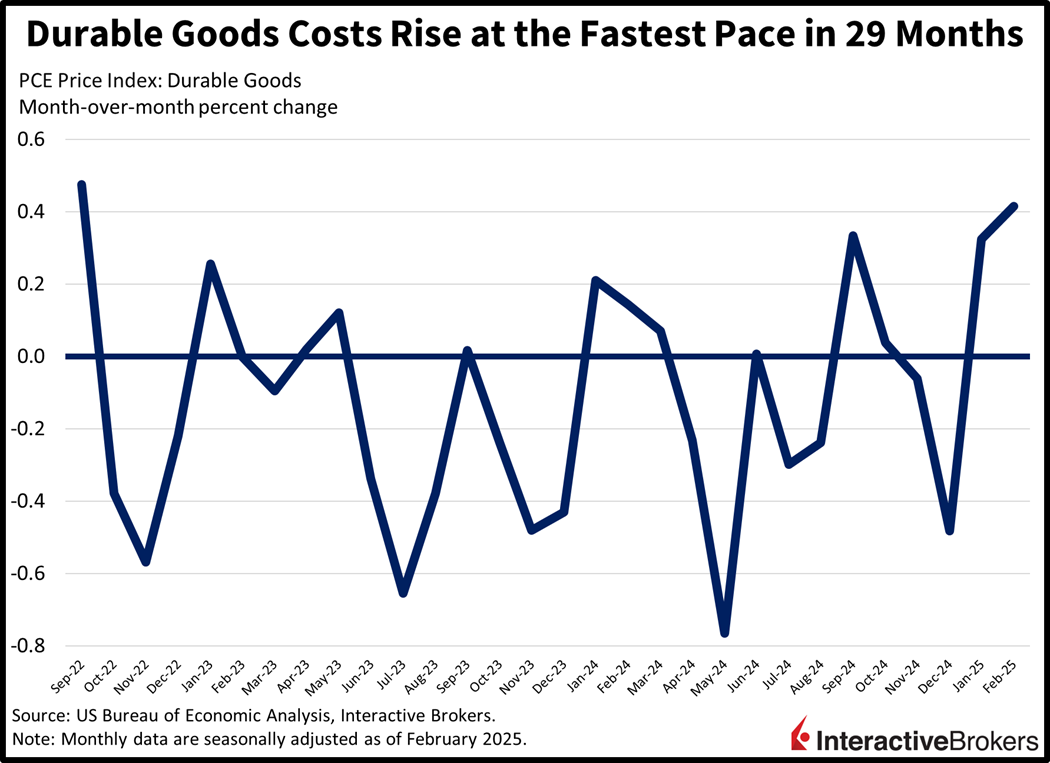

Goods Threaten an Inflation Pickup

Inflation trends in the report reflected an acceleration in durable goods and services costs that were partially countered by decelerating food and energy charges. The personal consumption expenditures (PCE) price index climbed 0.3% m/m and 2.5% year over year (y/y), as expected, and matched January’s results. But the core gauge, which excludes food and energy due to their volatile characteristics, increased 0.4% m/m and 2.8% y/y, a tenth of a percent loftier than the projection, which would have been unchanged from the prior month. The sharpest monthly increase in durable goods in 29 months, since September 2022, of 0.41% m/m, coincided with price increases of 0.4% and 0.1% across services and nondurable products. Food costs were flat, but energy goods and services rose 0.1%.

Past performance is not indicative of future results

Sentiment Gauge Revised Downward

An unfavorable revision to the University of Michigan’s Consumer Sentiment Index also weighed on investor psyche, with the March result being downgraded from 57.9 to 57. The sub-indices for current conditions and consumer expectations were updated in bifurcated fashion from 63.5 and 54.2 to 63.8 and 52.6. But inflation expectations were adjusted north, from 4.9% and 3.9% to 5% and 4.1% over the 1- and 5-year time horizons.

Investors Flock to Safety

Investors are rushing for the risk-off playbook as the outlook for earnings expectations and economic performance continue to diverge amidst substantial trade uncertainty. All major equity benchmarks are declining sharply with the Nasdaq 100, Russell 2000, S&P 500 and Dow Jones Industrial down 2.3%, 2.1%, 1.7% and 1.5%. All sectors are being sold except for the defensive utilities and health care areas; they are higher by 0.9% and 0.1%. Leading the laggards south are consumer discretionary, technology and communication services, which are losing 2.8%, 2.4% and 2.4% on the session. Folks are grabbing Treasurys aggressively, however, preferring the long-end, and the 2- and 10-year maturities are changing hands at 3.92% and 4.27%, 7 and 9 basis points (bps) lighter in trading. Softer borrowing costs and weak US data is weighing on the Dollar Index, which is trimming 26 bps as the American currency depreciates versus the euro, yen, yuan and loonie but appreciates relative to the franc, pound sterling and Aussie tender. Commodities are mixed, but safe-haven demand is driving gold up 0.9% whereas tariff worries are bolstering copper by 0.5% and plunging mortgage rates are helping lumber gain 0.2%. Silver and crude oil are lower by 0.9% and 0.7%, on the other hand.

The Long Game

Today’s data underscore how uncertainty itself can lead to faltering consumption, as household brace for potential disruptions ahead by closing the pocketbooks. While consumers surprised strongly by overcoming inflationary pressures and elevated interest rates prior to 2025, the additional headwinds of government spending reductions, tariff impacts and job security worries are proving too heavy for the US economy to handle. Against this backdrop, however, the Trump administration has raised its tolerance for financial market volatility and economic turbulence by adopting a short-term pain, long term gain framework. It’s certainly a risky endeavor to attempt to restructure international trade and trying to achieve some level of fiscal responsibility simultaneously, but don’t count this economy out just yet, because the tailwinds of lighter taxation, reduced regulation and manufacturing onshoring activities may save the day later in the year.

International Roundup

UK Posts Surprisingly Strong Retail Numbers

Retail sales in the UK expanded 1.0% m/m and 2.2% y/y last month, substantially exceeding expectations for a 0.3% m/m decline and a 0.5% y/y increase. The results compare to growth rates of 1.4% and 0.6% in February. Similarly, core retail sales, which matched the headline numbers, also surpassed expectations. Analysts anticipated contractions of 0.5% and 0.4% following January’s results of 1.6% m/m and 0.8% y/y.

CPI Climbs in Tokyo

Tokyo’s Consumer Price Index advanced 2.9% y/y in March, up marginally from 2.8% in the second month of the year, and the core version of the gauge moved north by 2.4% y/y compared to the analyst estimate of 2.2%, which would have matched February’s result.

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Bonds

As with all investments, your capital is at risk.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account